|

Keitai in Public Transportation. By Daisuke Okabe and Mizuko Ito: In an excerpt from their book "Personal, Portable, Pedestrian" by MIT Press, two professors examine the emerging do's and don'ts of public mobile phone use. First of two parts. [Japan Media Review] 12:44:50 PM |

|

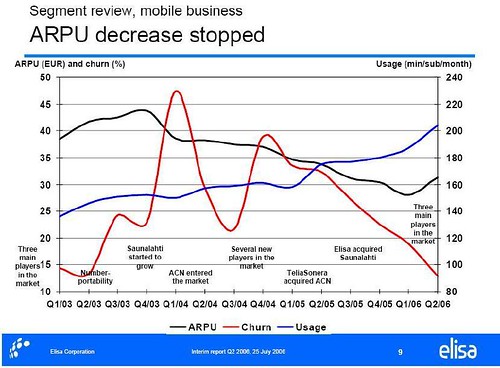

Finnish Bloodbath Finished

Elisa, a small Finnish operator

released its 2Q results today

. Most noticeable was the dramatic improvement in the mobile operations over the last twelve months.

- KeithJamesMc [TeleBusillis]

It is apparent that since the two big MVNOs, Saunalahti and ACN were bought out by Elisa and TeliaSonera the market has stabilised extremely quickly. Churn has fallen off radically and ARPU are now finally on the rise again. The Finnish market gives a big clue to all regulators throughout the world how to lower prices in a market ñ increase competition. In the UK, we have seen this effect with H3G UK cutting prices in the extreme, despite the huge sunk costs of the 3G licences. Iím sure that there are a few UK-based oligopolistís scheming how to take out the disruptive H3G and resume normal shareholder service. Also, it makes the decision of Teliasonera to launch Xfera in Spain ever more masochistic: they know the forthcoming world of pain and still insist on going ahead, strangeÖ 12:43:34 PM |

|

It's not personal, It's strictly business

In the late 1980ís Motorola taught Nokia a painful lesson in patents: it sued Nokia for GSM patent infringement in the USA and took the case to the International Trade Commission attempting to get the import of Nokiaís products to USA banned. Nokia quickly settled for US$20m, when US$20m was a lot of money for Nokia, and licensed Motorola's GSM technology. As a consequence, Nokia quickly established a company wide initiative to start patenting everything coming out of their labs, because they realized the patent process could be a legal means for negotiation and market leadership as opposed to a pure technical disagreement over invention. Prior to this, Nokia thought that short product cycles would render patents valueless.

- KeithJamesMc [TeleBusillis]When the 3G standard was being architected in the late 1990ís, Nokia and Ericsson tried to develop a European flavour of CDMA elbowing out Qualcomm and they were nearly successful with their efforts in the darkened ETSI rooms. However, Qualcomm taught Nokia a painful lesson in the power of Capitol Hill lobbying and ultimately got the US government to threaten a trade war with the EU. The US even sent a ìverbal noteî to the Finnish government threatening them not to go ahead with licensing 3G spectrum before the Intellectual Property Rights issues were resolved. Eventually everything was resolved by a deal being struck between Qualcomm and Ericsson. Nokia continued to haggle for a while, but eventually licensed the Qualcomm IPR with some GSM IPR in return. In 2006, as the adoption of W-CDMA is starting to kick-in and Qualcomm has changed the rules of the game from the late 1990s: it has sold the infrastructure and handset business and focused on technology licensing and chips, Nokia is yet again back at the negotiating table. The proxy war that Nokia is fighting in Brasil and India is frankly a joke : everyone knows the only reason that no-one can compete with Nokia and Motorola in ultra-low cost handset market is because they control the vital GSM patent pool together with the (current) scale advantage for GSM: Ericsson, Siemens and Alcatel have left the handset game and just collect the GSM royalties. Similarly, everyone knows that China will not license a 3G technology which will leave itsí incumbent equipment providers at such a huge disadvantage. Meanwhile, Nokia keeps on learning painful patent lessons with itsí failure to close out cross-licensing agreements . Is this just Nokia settling a couple of disputes before it enters the ring for the main bout? I think everything is bubbling up nicely for a quite a brawl: every follower of The Godfather Saga knows that as power is passed from one generation to another, more than a little blood is shed. 12:42:54 PM |

|

BSkyB -- Leveraging the Power of Content Free Cash FlowIn today's results to 30th June, Sky revealed it generated £563m of FCF in the year. This is after total capital expenditure of £212m (including £37m on LLU unbundling), but before £209m on the purchase of Easynet. Sky can easily afford itís capital broadband plans of £250m over the next couple of years (£130m -- fixed and £120m -- success based). It can also easily afford the £290 of cash operating losses.The scary thing for the competition is that the cash-generating part of the business is remarkably capex light. Sky only spent £212m on capex, of which £37m was on unbundling exchanges. Furthermore another big chunk of the capex (£38m) was spent on upgrading IT support systems which will be shared with the new broadband business. Transmission CostsOne thing that should frighten the Telcoís is how cheap Skyís transmission costs currently are: in 2006 they were £171m for the TV business which is flat year-on-year. Total transmission costs increased by £63m because of the Easynet network costs, which was only acquired at the beginning of January so yearly run-rate on the fixed network that Sky have acquired and building will probably be at around the same rate as the whole of the TV transmission, once the LLU build out is finished. If we conservatively just look at the DTH revenues, transmission costs are only 5.4% of revenues. If you consider the bandwidth that this delivers, this is an absolute huge advantage compared to DTT (Freeview), Cable or Copper.Content InvestmentSky spent £1.6bn on programming ñ this is huge barrier to entry to anyone thinking of entering the content business, especially when you consider the Sky bundling approach. The spend on Sport is the largest chunk of this is an incredible £766m ñ how anyone else in the UK can compete with this is beyond me. Sport is obviously the cornerstone that drives Sky forward. Movie costs were £310m which is in absolute decline (down £33m y-o-y and the lowest figure for six years). News & Entertainment costs were £200m, an increase of £20m because of an increase in own cost & commissioned programming. Third party channel costs fell to £323m (a drop of £39m) and the third party channel cost per subscriber is £3.37/month.The overall trend is what interests me: Sky is spending less with third parties and spending more on generating itsí own unique content, whether internal, (eg SkyNews) commissioned (eg SkyOne) or rights-based (eg exclusive Sports Rights). Digital Penetration ñ core business growthI don't think Sky's growth in its TV service is by any means complete:- First -- it is going to add new subscribers to Sky. Sky's targets around 400k a year which is about £156m/annum at current ARPU rates. I donít think this is a stretch at all and could quite easily grow the 500k per annum which would add £200m/annum  - Second -- there is big upselling opportunities on the base -- only 13% take up multi-room, HD has only just launched (again Sky are technologically in the lead) and there are the people who will upgrade the bundle (around 45% take Sports + Movies + All Channels) - Third, additional revenue streams such as Advertising Revenue will improve as audience share improves. Wholesale content seems to be stable which they attribute to Cable losing net premium customers. - Finally and this is where the telco's will be really envious -- Sky actually increases product prices on a yearly basis! Once you add up all the elements you could quite easily see Sky growing itsí core business revenues at 5-10% per annum. Sky's business model is also extremely leveraged so I can see profit and cashflow growing at a quicker rate (7.5%-15% pa) This is a nice business before you add in the home telephony and internet business, both of which should increase the value of the TV business through increased customer loyalty. 1% of churn reduction is £50m/annum saving in customer acquisition costs. DifferentiationIt is obvious that Sky are placing a big investment in customer care and home engineers and I suspect they are building a "digital walled garden" -- if you want the best quality, features and service join the Sky Club. Carphone Warehouse are obviously taking the ìvalueî dumb pipe approach and BT will like to play the Sky game, but donít have the content, but do have years of telco/internet experience lead and I suspect have a far more "less digital" customer base who love analogue TV and the BBC. I'm not sure where Orange is placing themselves or o2 once they join the playing field.I am also sure that Skyís EPG (Electronic Programming Guide) will be a critical differentiator in the Video camp. If Google is premier Gateway for information retrieval and MySpace is the premier Gateway for Social Networking, the Sky EPG will be premium gateway for video whether on the net or broadcast. This will be a big asset in the future. Murdoch SnrMurdoch Jnrís Dad gave an interview the other day and it is obvious that the BSkyB model will be replicated in Italy and the USA. His comments about commission rates for advertising on MySpace will have sent a shudder down the spine of Google. Iím almost sure that BskyB will not get any sort of exclusivity on Myspace content as it expands overseas. It is obvious that the whole of the Mudoch Empire is not thinking about convergence, but implementing it...Personally, I think BSkyB is looking the strongest going into the UK BroadBand Wars. - KeithJamesMc [TeleBusillis] 12:42:02 PM |

|

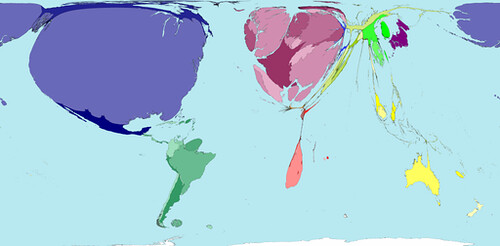

Where are the biggest wallets?

Have you ever wondered where in the world to launch a premium product?

- KeithJamesMc [TeleBusillis]This map gives a big clue. Courtesy of the wonderful WorldMapper Research Project .

In 2002, 53 million people in the world lived in households in receipt of US$200 purchasing power parity (PPP) per day. Of these high earners, 58% lived in the United States.Now remind me again, why should Vodafone sell out of Verizon Wireless? 12:38:31 PM |

|

What's Wrong With Yahoo Germany?. A good story about Yahoo’s prospects in Germany, and why it is not doing so well there. While Yahoo’s revenue growth has accelerated by double-digit percentages in most European countries, Germany has chugged along in first gear since 2000, Dominique Vidal, head of Yahoo Europe said. He blames a lack of competition for depressing growth there. 11:44:14 AM |

|

News Corp Jamboree This Weekend. And the media is going ga ga over it…the News Corp retret at Pebble Beach is its biggest and most high-powered ever: LAT says that the event will include such political powers as British Prime Minister Tony Blair, former President Clinton and Israeli Vice Premier Shimon Peres. Los Angeles Police Chief William J. Bratton will opine on remaking complex organizations, former Vice President Al Gore will riff on climate change, and U2’s Bono will deliver a keynote address titled “The Power of One. 11:42:43 AM |

|

News Corp Jamboree This Weekend. And the media is going ga ga over it…the News Corp retret at Pebble Beach is its biggest and most high-powered ever: LAT says that the event will include such political powers as British Prime Minister Tony Blair, former President Clinton and Israeli Vice Premier Shimon Peres. Los Angeles Police Chief William J. Bratton will opine on remaking complex organizations, former Vice President Al Gore will riff on climate change, and U2’s Bono will deliver a keynote address titled “The Power of One. 11:42:09 AM |

|

1.5 billion wireless handsets to ship in 2011.  Just when we all thought that 400 million handsets shipped globally in a year would be plenty, the consulting company Analysys has predicted that 1.5 billion (with a "b") handsets will ship globally by the year 2011, a mere five years away. Just when we all thought that 400 million handsets shipped globally in a year would be plenty, the consulting company Analysys has predicted that 1.5 billion (with a "b") handsets will ship globally by the year 2011, a mere five years away. Tag:smart phones | Posted in: Specific 3G News Devices Our 3G Support Service - 3G Devices [The 3G Portal 3G News Feed] 11:34:20 AM |

|

Mastering New Marketing Practices. Last month, I had the pleasure of addressing a CMO Summit held in New York. I was given 15 minutes to set up a discussion on the future of marketing. It forced me to be even more concise than usual,... [Edge Perspectives with John Hagel] 11:31:29 AM |

|

Mobile Industry Booming Japan. MobileIndustry.biz, 22 July 2006 A new report by Japanese business site Tech On has revealed that Japan's mobile industry is booming - and that mobile gaming is on the rise, too. According to the report figures released by the Ministry of Internal Affairs of Communication state that the mobile industry has grown to 722.4 billion Yen (4.9 billion Euro) over the past 12 months - a rise of 39 per cent. [Wireless Watch Japan] 11:29:52 AM |

|

Adobe Japan Plans Revolution. Yomiuri, 24 July 2006 Adobe, which was established in 1982, has 54 overseas offices and more than half its revenue comes from outside the United States. Japan accounts for about 20 percent of revenue, positioning itself as the second-largest country in these terms. It boasts advanced mobile devices and is likely to continue to be one of the strategic markets for Adobe as the company has increased efforts to push its products to mobiles. [an interesting interview with the incoming president of Adobe Japan -- Eds] [Wireless Watch Japan] 11:28:22 AM |

|

NEC, Panasonic and TI Form Handset JV. PR Newswire, 27 July 2006 NEC, NEC Electronics, Matsushita, Panasonic Mobile Communications and Texas Instruments just announced that the five companies have signed an agreement to establish a new joint venture company. The company will conduct global development, design, and technology licensing for a hardware and software communications platform to manage the core communications functions for 3G handsets. The new company, Adcore-Tech Co., Ltd ("Adcore-Tech"), is scheduled to be established in August, 2006 at the Yokosuka Research Park in Yokosuka, Japan, with approximately 180 employees. (As we stated on Tuesday this week: "expect a formal announcement in the coming days." -- Eds.) [Wireless Watch Japan] 11:25:58 AM |

Last update: 8/5/06; 4:54:18 PM .

![]()

![]()

![]()

![]()