|

Complex Phones Confuse People. If you have used some of the newer fully featured phones currently on sale, then you have experienced the frustration that comes with feature creep. Poor battery life, user interfaces to make you want to jump off the Brooklyn Bridge (Moto, are you listening?), complex PC-to-phone music transfer process … and did we mention tinny headphones, and poor battery life.

Even gadget junkies likes myself often opt for the simple please of just a phone. (Nokia 6101 is my favorite for days when I just want a phone.) In case you had doubts, there is a study to prove this.

Style was mentioned as a buying factor by 39 percent of the users, making it the single most popular answer, but cost considerations were the biggest reason overall

The study conducted by J.D. Power and Associates in essence says that for U.S. consumers price and looks, are more important than advanced features. However, if the phone’s advanced features were dead simple to use, then consumers started using them, the study says. Learn from Steve Jobs people!

3:58:46 PM |

|

Google, MTV & Superdistribution. Back in April in a piece titled "SocialNets -- the Power of the URL", I wrote:

"Like every media revolution in history, when tectonic shifts occur on the production side of content, equally disruptive shifts follow in distribution (or visa versa). What we're experiencing now is no different. Not only do these (consumer-generated) URLs mean that consumers are now "producers", they are also being used as a new channel for media distribution[base ']Ķ the consumer is also becoming a [base ']Äúdistributor[base ']Äù… Over the next few years, new ventures will emerge to monetize such new distribution opportunities, and they will more directly compensate people for the role they are playing as filters and distributors of media.

Google's joint venture with Viacom's MTV, announced this week, provides a watershed moment in the scenario depicted above. Google's Adsense represents one of the largest web-based content syndication platforms in the world, and the fact that MTV will begin to use it to distribute video programming out to the edges marks a breakthrough in a business model known as "superdistribution".

A key facet of superdistribution is the willingness of the content/copyright owner to compensate each player who functions as a redistributor of digital media. For instance, bloggers who participate in Google's Adsense network will now be able to earn income as a redistributor of MTV's video content.

To go back to our original post again,

Since the Internet does away with the need for physical packaging of content (e.g. DVDs, CDs, newsprint, etc.), the need for specialized distribution outlets goes with it. Looking out several years, it's not too difficult to envision a media landscape where the majority of traditional media distribution outlets reliant on the benefits of natural monopoly economics have largely been replaced with a highly-fragmented layer of people-powered community-based distribution networks.

At the end of the day, Google's deal with MTV will prove hugely disruptive, as people-powered superdistribution begins to transform the way Hollywood products are discovered, delivered and consumed. And not surprisingly, Google will be the center of gravity of this new digital media universe.

Now, if I could convince/help them buy Lions Gate Entertainment, the stage would be all set for Google to become one of the first "socially-integrated" media empires of the the 21st century -- one that could leapfrog Rupert Murdoch's News Corp.

Robert Young is a serial entrepreneur who played a major role in the invention & commercialization of the world's first consumer ISP, Internet advertising (pay-per-click ads), free email, and digital media superdistribution.

3:57:32 PM |

|

Google to Invest $1 Billion In India. A few days after in announced plans to set up a R&D Center in China, Google has now decided to invest up to $1 billion on a back office in Indian state of Andhra Pradesh, according to news reports. The proposed center, which the Indian government just approved, will likely be spread over a million square feet in what is called a ’special economic zone’ in the southern state. Dell’s and Accenture’s investments were also given the go-ahead.

Google currently operates a development center in Bangalore. Google’s India office was responsible for coming up with Google Finance. About half a dozen technology companies have announced plans to invest a billion dollars or more in India

3:48:49 PM |

|

Mobile TV - It's a hit. Mobile Monday Melbourne.

I opened with the statement that "Mobile TV" is not about "TV" on the mobile.

To read my opinions on "fad or fantatasic", "why bother", "winners and losers", "if so hot why so slow?" and more download the PDF of the presentation. I've also prepared a 2-page (PDF) easy-to-read discussion, which was a answer to a panel question.

My bottom line?

For more insight see this article which I just found today Mobile TV and Wi-Fi® On a Single Chip and I nearly jumped out of my seat as it spells out one of my key messages, read the last paragraph:

Is there an i-mode project or news that you think we should feature? Email tips@imodestrategy.com. Thanks! [i-mode Business Strategy] 3:47:31 PM |

At Melbourne Mobile Monday's August 7 meeting I spoke about Mobile TV - "Mobile TV [base ']Äì It[base ']Äôs a Hit!".

At Melbourne Mobile Monday's August 7 meeting I spoke about Mobile TV - "Mobile TV [base ']Äì It[base ']Äôs a Hit!". this requires device intelligence and the cellular feedback loop. Those 3I 3Cs are where the profit is and where the whole purpose of the mobile content industry is heading.

this requires device intelligence and the cellular feedback loop. Those 3I 3Cs are where the profit is and where the whole purpose of the mobile content industry is heading.

|

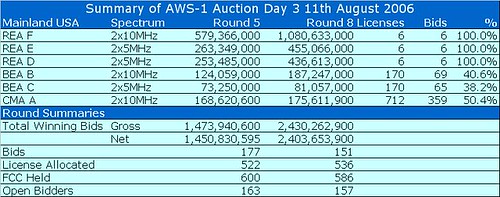

AWS-1 Auction ñ Day 3 Summary

Another day, another US$952,823,305 into the US government coffers.

- KeithJamesMc [TeleBusillis]

The price of a mainland US licence in the ìFî band has crossed the threshold of US$1bn. The price differential between the equivalent ìAî band and ìBî band is growing huge at 6.15x and 5.77x. It is difficult to analyse bidder intentions during the progress of an auction because some of the moves may just be bluffs. It is akin to analyzing a poker game without the privilege of seeing the hands that the players hold. Mind you, the Monday Morning Quarterbacking that goes on post-auctions is also fraught with difficulties as people re-invent history and intentions to prove that they are brilliant after all. It is almost as if everyone takes a cognitive dissonance pill on the night of auction exit and wake in the morning with a whole new view on the world. I think Verizon Wireless and Atlantic Wireless are exhibiting strange behaviour. First of all, Verizon Wireless is bidding on every supa-region of mainland USA in the ìFî band except the North East. Atlantic Wireless is similarly only bidding in the ìFî band and only on the North East region. Each is just bidding by the minimum increment each round. This is probably just a weird statistical freak because collusion is not permitted. Atlantic Wireless is a new company which qualifies for the 25% discount for new entrants and reputedly is financed by the same people behind Aloha partners who already hold some spectrum in the WiMax bands. In 2000, one of the Verizon Wireless partnership, Vodafone, employed a similar tactic in the UK 3G auctions. Everyone knew before the start of the auction that Vodafone was by far and away both the strongest financially and had the biggest market share in the UK. Vodafone just sat on the license with the highest amount of available frequency (30MHz) and let the rest of the incumbents fight for the remaining 20MHz licenses on offer. Vodafone never budged from the 30Mhz license during the auction process. If it wasnít for BT who was determined to force Vodafone to pay a realistic price for the extra spectrum, Vodafone would bought the extra frequency at a big theoretical discount. In the end Vodafone got the license at between 1.47x and 1.49x the price of the smaller licenses. Only time will tell whether Vodafone bought too much frequency but the Monday Morning Quarterbacks who egged all the bidders on during the auction now claim all the bidders were idiots who vastly overpaid. There was also a rather grand gesture by T-Mobile this evening in Round 8 who bid more than the minimum (a 20% increase) on every ìFî license that it was permitted to bid on and therefore won every bid. Personally, I think the tactic is so that T-Mobile will be featured in all the weekend press as the auction leader. Also, it meant the total spend of T-Mobile was just over a headline grabbing US$1bn. T-Mobile isnít bluffing me ñ it is desperate for the extra spectrum and will pay whatever is necessary. The T-Mobile mothership, Deutsche Telekom, announced on Thursday that USA cash flow was around US$1bn for the first six months of the year. All of this is at risk if T-Mobile doesnít buy enough spectrum to launch next generation services in the key US markets. Therefore, T-Mobile will continue bidding until enough people pull out and leaves it with the necessary spectrum. Then the T-Mobile and Deutsche Telekom executives will breathe a huge sigh of relief and hope that too much damage hasnít been done to the shareprice of the mothership. Rather than the Peacock-esque behaviour of the mega-bidders, the more interesting fights at this early stage are breaking out in the rural areas. Iíll try to look at some of smaller players over the weekend. 3:39:18 PM |

|

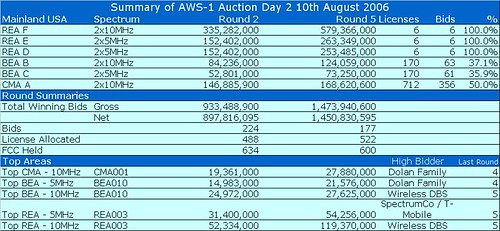

AWS-1 Auction ñ Day 2 Summary End of Day 2 and the US government is US$553,014,500 richer or less poor depending upon your personal way of thinking about the US deficit.  We witnessed the departure of 5 companies from the runners and riders to leave 163 still bidding. PCS Partners, L.P. (US$3m upfront payment), Hawaiian Telcom Communications, Inc. (US$2.155m), Leaco Rural Telephone Cooperative Inc (US$712.5k) and Arapahoe Telephone Company d/b/a ATC Communication (US$136k) all exited without making a single bid. If anyone can explain the rationale of going through the whole FCC procedure of registration and actually making a deposit without even bothering to make a single bid, Iíd be extremely interested to listen. Yes, they are going to get their deposits back but it all seems a nihilistic existence to me. At least Craw-Kan Telephone Cooperative, Inc. (US$434k) bid on five licenses in Round 1 and then saw that they faced a minimum of two other bidders on every license and used their proactive waivers to see how the bidding developed before calling it a day in Round 5. CenturyTel who outbid Craw-Tel on two rural licenses are probably the story of the auction so far. CenturyTel placed a huge US$59m deposit with the FCC which was the 11th largest and is now left bidding on a mere US$9.162 ìbidding unitsî having automatically lost 2 waivers because of low activity in round 1 & 2. CenturyTel currently have the winning bids on 32 licenses at a total price of $7.7m. I feel CenturyTel have paid a much bigger deposit than necessary and probably have a really poor bidding strategy. The heavy hitters have followed the same course as yesterday. If everything continues on Friday as the first two days, Iíll be able to reveal what I think is the first ìsignalî and furthermore place it in a historical context with the infamous UK 3G auction of Mar-Apr 2000. - KeithJamesMc [TeleBusillis] 3:32:21 PM |

|

AWS-1 Auction - Day 2 Observation 1

There is currently reluctance for the big players to bid on the smaller CMA and BEA licenses.

- KeithJamesMc [TeleBusillis]For an illustration of the problem, look at the Top 50 markets represented by CMA001 to CMA050. 26 of these licenses currently have no bid. Los Angeles has had 2 rounds of bids and only 1 ñ New York have people bothered to bid in every single round. All of the other 22 licenses have only had 1 bid. T-Mobile is in the lead in 19 of the markets having bid in round 1. The reason for the reluctance for bidding is explained on a small scale with this example from Hawaii. Say you want 20MHz in Hawaii and bid $100m in the REA008-F, someone in the next round bid $110m for the spectrum, but you notice that the cumulative bids on CMA050 ($20m), CMA385 ($10m), CMA386 ($10m), CMA387 ($10m) are only $50m so you place a bids on each of the individual licenses. As the bidding evolves the price of CMA050 rises to say, $150m, whereas the total price for the region rises to $160m. This is perfectly rational if the bidders value the ìruralî areas of Hawaii at next to nothing. It could also mean that you could be left with ìstrandedî licenses in the rural areas which are only worth something when ìbundledî together with the major license CMA050.It will be interesting to see when the big players (ie Cingular, Verizon, T-Mobile and Wireless DBS) stop bidding on REA-F licenses and start moving into the smaller pool. This will be some sort of signal that they believe the value of REA-F has peaked. For some like Wireless DBS, it may be pointless actually owning the smaller licenses as the value is only if then have spectrum which they can offer to all itsí base, hence the reason it seems to be the only major bidding in Alaska.... 3:02:31 PM |

|

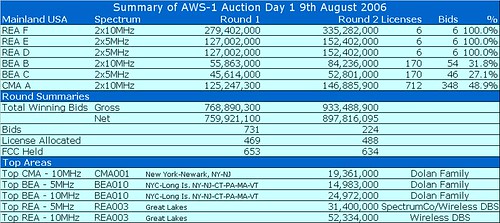

AWS-1 Auction ñ Day 1 Summary

Two rounds into the expected marathon auction and the sparring has begun, no-one has landed a heavy punch and certainly no blood has been drawn yet.

- KeithJamesMc [TeleBusillis]

As expected there is a lot of action around the Regional Licenses with everyone who can be bothered bidding at this early stage placing the minimum amount. ï Verizon Wireless has only bid on the big F Block, but not in their original home turf of the North-East; ï Cingular is also focusing on the big F block, adding Hawaii to mainland USA and also experimenting with the BEA blocks for Chicago and New York; ï T-Mobile is bidding in all the Regional Blocks and also a few of the main metropolitan areas in the BEA and CMA bands; ï Wireless DBS is also only bidding on the Regional Blocks; ï Perhaps the only surprise is that SpectrumCo (ie the Cable companies) are bidding on the big regional licenses rather than their home turf. Also, there seems to be a lack of initial interest in the smaller blocks with a lot of the big metropolitan areas not having received a single bid yet. But there is a long, long way to goÖ 3:00:15 PM |

|

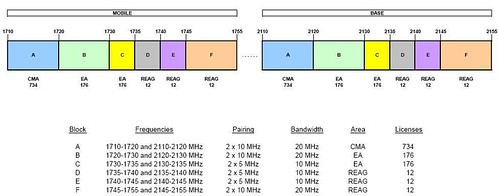

AWS-1 Auction 66 Two days to go and Iím getting pretty psyched ñ all the ingredients are prepared and thrown into the mixing bowl - I'm ready for a fiercely fought and therefore expensive auction. Frequency Band This is not the same frequency band as the UMTS spectrum licensed in Western Europe and Japan. So dual-mode phones will be needed for UMTS roaming services to work cross continents. Personally, over time this is not a big problem as quad-band GSM phones have overcome this problem in the past. Iím sure that the proportion of total Bill of Material cost for this extra functionality will be minimal in the overall scheme of a multi-baseband 3G phone. Anyway, the US internal market is so big who really cares about roaming? Iím sure that some companies will be considering deploying non-standard 3G technologies (ie apart from EV-DO and UMTS) ñ hopefully, we may see some companies trying to deploy OFDM based technologies. Market ConsolidationThe argument goes that as AT&T Wireless and Nextel have disappeared as independent companies from the market then there will less demand for the spectrum. I really, really doubt it. Spectrum is the oxygen that wireless companies breathe: the more they have the more things they can do. Any new entrant wanting to offer a wireless service using exclusive spectrum has to compete in these auctions: otherwise they have to rely on unreliable unlicensed shared spectrum. More importantly, after all the expense of consolidation, Iím 100% positive that the huge wireless companies will pay huge premiums (in the form of license fees) to keep their club as small as possible: Verizon Wireless, Cingular and T-Mobile will fight to keep anyone else from owning a nationwide license and more importantly to keep potential customers out of the key Top 10 markets. Sprint is a more complicated matter and more of that later. Potential ìOnce in a Lifeî Opportunity All other previous spectrum auctions have been based upon a patchwork of licensees across the USA covering as many as 714 areas or at a minimum 176 licenses. Although this policy has allowed the emergence of small rural providers, it has meant that not [TeleBusillis] 2:48:57 PM |

|

Sprint Races Ahead, Chooses Mobile WiMAX For 4G.

Since its merger with Nextel, Sprint’s been sitting on a huge amount of 2.5GHz spectrum across the US, and its long-held intention has been to use it to build out a nationwide mobile broadband network. After testing or evaluating nearly every suitable technology out there, the company announced today that it will use mobile WiMax, giving the technology a huge boost. Sprint plans to roll its network out by the end of 2007, with more significant coverage in 2008, offering download speeds of 2-4 Mbps (which sounds like a welcome dose of reality to all the grandiose claims about WiMax we’re usually treated to). Despite a lot of speculation that Sprint would choose either Qualcomm/Flarion’s Flash OFDM or IPWireless’ UMTS TD-CDMA (which probably didn’t deserve to win solely on the basis of that acronym), mobile WiMax looks to be the right choice for the company. Its executives used the word “ecosystem” several times to describe the environment surrounding mobile WiMax, and Bin Shen, the company’s VP of broadband strategy, reiterated the point on a conference call with me: Sprint wanted to choose a technology based on an open standard that invited and allowed for competition, to help drive costs down throughout the network, from chipsets to network equipment to devices; it also wanted a standard that would be widely adopted. Part of what makes this the right decision for Sprint is that with this choice, it’s made a significant step towards creating a mobile WiMax market, and will certainly influence other operators to take a strong look at the technology. It’s also given itself a strong leadership role in mobile WiMax’s continuing development — for instance, it’s working through the WiMax Forum with other operators to define a “Wave 2″ profile of the technology to meet its desires and demands. There’s some unspoken subtext here, too though: The idea of adopting a second technology, in addition to CDMA, that’s controlled by Qualcomm probably wasn’t particularly attractive. The big Q’s royalty system hasn’t won it a lot of friends (apart from happy investors), and it’s currently experiencing some discord with operators in emerging markets who feel its royalty demands, particularly on mobile handsets, and chip pricing inhibit their ability to compete with their GSM rivals. WiMax addresses all those factors — the technology isn’t controlled by a single entity, and nobody holds a commanding about of the IP behind it. This means there’s going to be a lot more competition, and Sprint’s fortunes won’t be as tied to one outside company. Some other interesting points: Shen talked about how the WiMax network will be complementary, both to Sprint’s existing cellular networks, but also to fixed broadband networks, particularly those of the cable TV companies it’s partnered with. He said that the carrier wants WiMax chips in its devices to also support Wi-Fi, while it’s focusing on creating a network whose real value is in mobility, not necessarily in fixed wireless usage. Also, he mentioned billing access to the network on a per-household basis, rather than per device — this will be necessity if Sprint and it’s vendors’ vision of millions of connected electronic devices is to come true. It’s also an interesting pricing model that could shake up mobile operators a bit. Without a doubt, Sprint has quite an undertaking before it, not the least of which convincing investors unhappy with its recent results that it’s worthwhile to drop a few billion on a new network with a somewhat unproven technology when it’s also upgrading its existing EV-DO network. The new network is being pitched as a data network that will connect all sorts of electronic devices, rather than a straight replacement for EV-DO, which will still be used to provide voice functionality. Key to its success will be getting WiMax into those devices, but also coming up with applications and services people will want to use. Sprint does enjoy the highest data spending of US operators, but on the whole, mobile carriers haven’t done the greatest job in developing compelling uses for their networks — for instance, it was slightly disheartening to hear Sprint’s CEO go through several scenarios based on video calls or video chat, given that’s something telecoms have tried to introduce so many times with so little success. But by expanding connectivity beyond mobile phones and into other devices, I’m optimistic that the WiMax network will serve as an open platform that electronics manufacturers and developers can use to craft their own services and apps. I’d also venture this sets the stage for some sort of more detailed tie-up between Sprint and a South Korean operator. SK Telecom has been expanding overseas, and is the likely candidate, given its role in MVNO Helio, which uses Sprint’s network, as well as its expertise in both EV-DO and WiBro, a variant of mobile WiMax. One final point: you have to love the timing of this big Sprint announcement, the day before the FCC kicks off its huge spectrum auction. I’m guessing this isn’t a coincidence, but rather a reminder to all the would-be entrants to the wireless business of both the investment required to build a nationwide network, and also that the incumbents aren’t going to sit idly by as they roll out their flashy new networks. We’ll see if it scares anybody off. Technorati Tags: mobile, sprint, nextel, wimax, wibro, 4g, qualcomm, intel, samsung, motorola 2:47:40 PM |

|

Nokia's music move makes sense as 3G drives music downloads.  Annual mobile music revenues will top $14bn worldwide by 2011 - according to the latest report from Juniper Research. This change is courtesy of OTA full track music taking off, as 3G networks and 'music' handsets become more globally accessible and business models evolve, allowing consumers to purchase both PC and mobile music in a single transaction. Prominent market drivers for the acquisition of full track music are likely to be the dual download facility, increased bandwidth offered by 3G networks and the evolution of the mobile handset into a multi-purpose communications and entertainment device.

Annual mobile music revenues will top $14bn worldwide by 2011 - according to the latest report from Juniper Research. This change is courtesy of OTA full track music taking off, as 3G networks and 'music' handsets become more globally accessible and business models evolve, allowing consumers to purchase both PC and mobile music in a single transaction. Prominent market drivers for the acquisition of full track music are likely to be the dual download facility, increased bandwidth offered by 3G networks and the evolution of the mobile handset into a multi-purpose communications and entertainment device. Tag:mobile music | Posted in: Specific 3G News Business case Our 3G Support Service - 3G Applications [The 3G Portal 3G News Feed] 2:45:43 PM |

|

Mobile Advertising Provider In India A Good Idea - Business 2.0. Business 2.0 lists the creation of a mobile ad network for India as one of the 12 startups to launch now. The elaboration takes Ashu Mathura’s three person, Amsterdam based mobile advertising startup called ‘Mads‘ as an example and quotes Mathura as saying that there is an even greater opportunity for replicating this business model [...] [ContentSutra] 2:43:33 PM |

|

Tiscali UK To Merge With IPTV Player Homechoice. So the straight buyout hasn’t happened, though a variation of it has, after news leaks on this deal over the last week or so: Italian Internet firm Tiscali will merge its UK operations with UK IPTV pioneer Homechoice to increase the content it provides to its clients. 2:33:54 PM |

Last update: 9/12/06; 4:12:50 AM .

![]()

![]()

![]()

![]()